5 Essential Questions for EU-Exporting Companies Regarding Carbon Border Adjustment Mechanism (CBAM)

As the Carbon Border Adjustment Mechanism (CBAM) comes into play, companies exporting to the European Union must prepare for stringent regulations that could significantly impact their operations. CBAM aims to impose carbon tariffs on carbon-intensive products to prevent carbon leakage and drive global decarbonization efforts. In this article, we explore key questions board members should ask their top management to ensure readiness for CBAM and align with broader sustainability goals.

What Is CBAM?

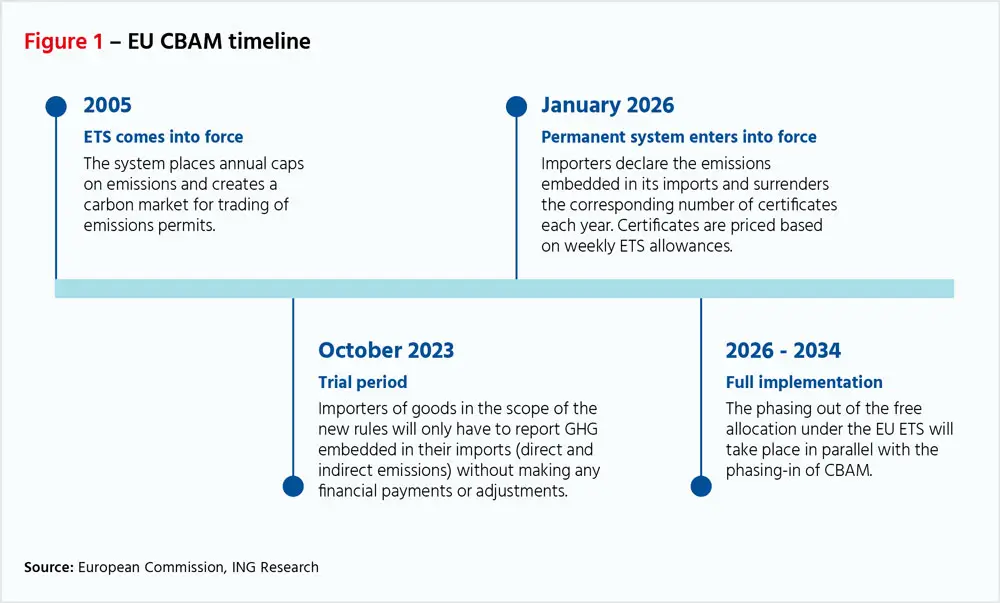

Carbon Border Adjustment Mechanism (CBAM) is designed to level the playing field for EU producers by imposing a carbon tariff on certain imported goods. This initiative targets products like steel, cement, aluminium, fertilisers, and electricity. By 2026, CBAM will fully implement its definitive regime, with a transitional phase running from 2023 to 2025. This mechanism is a critical step toward achieving carbon neutrality by addressing the carbon footprint of imported goods.

Q1: What Is Our Company's Readiness for CBAM Reporting?

The first step for any company is to assess its readiness for CBAM reporting. Companies that produce CBAM-relevant goods will need to report to the CBAM Transitional Registry every quarter. This requires proactive data collection and management, ensuring that all necessary information is available and accurate. Board members should inquire about the current status of these preparations and the measures being taken to streamline reporting processes.

Q2: How Will CBAM Impact Our Supply Chain and Costs?

CBAM will undoubtedly affect supply chains and cost structures. Companies need to understand how the cost of raw materials and exported goods will change under CBAM, including potential cost pass-throughs from suppliers. This analysis should also consider the broader implications for product pricing and competitiveness. Additionally, exploring alternative sourcing strategies and engaging in life cycle assessments could help mitigate some of these impacts.

Q3: Have We Identified Our Reporting Obligations Under CBAM?

It is crucial for companies to determine whether their products fall under CBAM's purview. This involves reviewing the list of CN codes in Annex I to ascertain if the products exported to the EU are subject to CBAM reporting. Even if a company does not have direct reporting obligations, it may still need to assist customers who do, particularly in calculating the embedded carbon in their products.

Q4: What Steps Are We Taking to Calculate and Reduce Embedded Emissions?

With the EU's deadline for using default values of embedded emissions set to expire on July 31, 2024, companies must develop robust methods for calculating actual embedded emissions. This process can be complex, requiring close collaboration with suppliers and the adoption of advanced carbon accounting software. Board members should inquire about the specific steps being taken to collect this data and reduce embedded emissions, ensuring alignment with CBAM requirements.

Q5: What Strategies Are We Implementing to Reduce Our Carbon Footprint?

CBAM not only requires transparent reporting but also encourages actual emissions reductions. Companies must adopt comprehensive strategies to lower their carbon footprint, including energy efficiency initiatives, renewable energy adoption, and carbon offset programs. Board members should seek to understand how these strategies align with CBAM requirements and how they will impact the company's overall sustainability reporting in India, particularly concerning emerging trends in sustainability worldwide.

Conclusion

As CBAM regulations take effect, companies must conduct a thorough evaluation of their preparedness. This involves understanding reporting obligations, analysing the impact on supply chains and costs, and implementing effective strategies to reduce embedded emissions and carbon footprints. With the complexities of CBAM compliance, companies that proactively address these challenges will be better positioned to meet regulatory requirements and build a competitive advantage in the evolving landscape of environmental sustainability.

At Oren, we assist companies across various industries in navigating the intricacies of CBAM and other sustainability reporting standards, helping them achieve compliance while advancing their sustainability goals.

About the author

Abhirup Das

Head of ESG & Sustainability Advisory

Abhirup leads Oren’s ESG & Sustainability Advisory practice, blending industrial engineering, digital transformation, and ESG governance to translate compliance into long-term financial and strategic value.